QR-payment software scale-up me&u recently announced that they closed a $30M fundraising round back in December 2022 and in more recent weeks it’s been revealed that there’s a merger on the table between me&u and their main rival Mr Yum. It made us wonder, how do the two companies actually differ? And, who’s ahead in the race to dominate the QR code ordering category?

Background

Mr Yum and me&u were both founded in 2018. Like any good Aussie rivalry - me&u set up its headquarters in Sydney, while Mr Yum calls Melbourne home.

Some may have thought the founders of both companies had crystal balls that foresaw the huge potential for their technology to take off amidst the COVID-19 pandemic, but obviously, this was not the case. The beginnings of these companies were more likely instigated when Apple introduced the ability to scan QR codes via an iPhone camera in its September 2017 iOS 11 update.

Despite starting around the same time, the founders came from very different backgrounds. Founder of me&u, Stevan Premutico previously founded restaurant booking platform, TheFork, which was later acquired by TripAdvisor in 2014 for $140M and before that worked as a Marketing Manager for Hilton Hotels. On the other hand, co-founder of Mr Yum, Kim Teo has publicly stated that her team were ‘underdogs’ on this front, with limited connections in the hospitality industry.

Products

To the average punter heading to their favourite cafe, restaurant or bar, the products from both companies appear and operate almost identically.

The customer sees a plastic circular beacon with a QR code on it in the middle of their table, scans it and proceeds to view, order and pay for items from the menu on their phone via the web (not an app). The platform not only shows them tantalising pictures of the food and drinks on offer but is also dynamically optimised as it receives ordering data to increase the opportunity for upsells.

It’s not surprising that both companies focus much more on differentiating themselves for the venue owner; the ultimate buyers of the software.

The proposition from both companies is centred around how the product integrates with the venue’s back-end operations, providing data for financial management, customer insights and marketing purposes. It’s on this front that you can see a more distinct difference in approach and execution.

Mr Yum leans into messaging around creating a better customer experience inside and outside the venue, and in turn increasing customer loyalty, while me&u is laser-focused on the promise of extra revenue (i.e. increased average order value) and makes a point of highlighting their founding roots in the hospitality industry.

Key messages from both companies' websites, demonstrating the nuance in their unique selling propositions:

Mr Yum’s promise to venues:

On average, Mr Yum venues see spend per head increase by 33%, acquire 3x guest data, and benefit from 41% more return visits.”

“Better serve, connect with and reward guests”

me&u’s promise to venues:

“Customers spend 30% more on average when they order with me&u”

“Built for hospitality, by hospitality”

This approach also plays out in the apparent functionality of each product and its current target buyer segments. Mr Yum is much more focused on becoming the “ultimate growth toolkit” for hospitality businesses, with more options to integrate with marketing tools. Their acquisition of hospitality CRM software company MyGuestlist in 2022, as well as the launch of an offering directed at marketing agencies (called ‘Connect’), demonstrated a doubling-down on this focus. These capabilities are likely more attractive to businesses with a customer base that cares about personalised experiences; they want their local cafe or restaurant to let them know their favourite dish is back on the menu, and remember that they don’t like spicy food but love a pinot noir when they arrive for a booking. Think of your typical trendy, boutique-style cafes and restaurants with sleek branding and staff you want to be friends with (but not in a creepy way).

By contrast, me&u offers a more pared-back offering and generally seems to be going for the “no bells and whistles” approach with less complexity, particularly on the marketing integrations front. This is an offering better suited to businesses less concerned about personalised customer marketing initiatives or providing a carefully curated customer experience, and more on preserving their inherently small margins by improving business efficiency. They want to keep up with customer expectations by implementing the latest tech, but the business bottom line is the priority. This would explain the company’s greater focus on attracting large-scale venues such as pubs as its primary customer base. Customers of these venues are less concerned about receiving regular updates about changes to the menu of their local watering hole - they just want to know that when they rock up they can get a good value chicken schnitty along with fast, hassle-free service.

It’s unclear from the outside how much the companies differ on pricing, as they both require a meeting/ demo to access this information and likely offer custom pricing deals to larger enterprise customers, such as the ALH Group who closed a big deal with me&u last year.

If you have any insights to add to this deep-dive, reach out to me at [email protected]! I’d love to include it in a future update.

Marketing

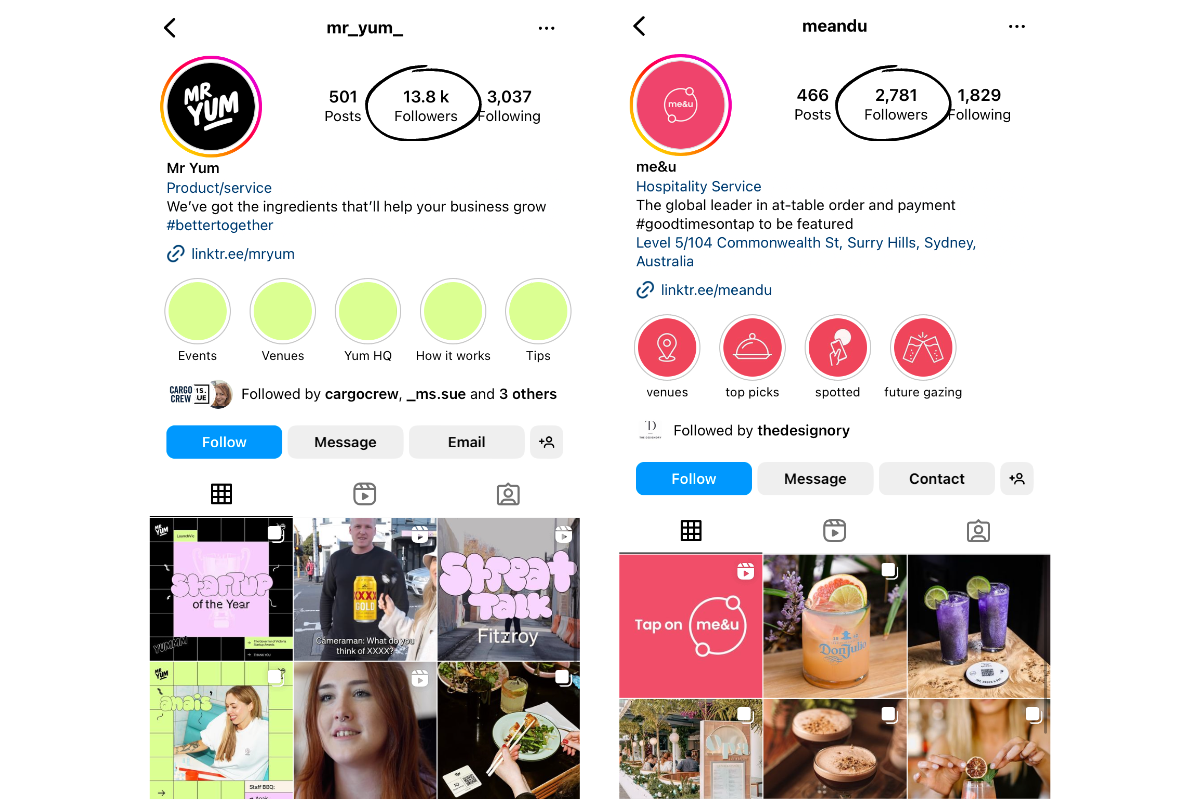

Another clear difference between the rival companies is in their approaches to growth. Since its launch, Mr Yum has clearly prioritised brand-building and broader awareness campaigns, with users (restaurant-goers) as well as buyers (restaurant owners). They have, in essence, ‘walked the talk’ when you consider their focus on brand-building capabilities through their product features. This was likely to make up for their lack of industry connections, helping them sell a narrative to buyers of - “users love us, so if you use our product, they’ll love you”. Aside from the aesthetic elements of the two brands which clearly distinguish Mr Yum as the more ‘trendy’ option, a quick comparison of their Instagram followings (see below), highlights this difference in approach.

On the other hand, me&u has clearly taken a more sales-led approach to growth, seeking out larger hospitality groups to sell into and roll out their product at scale. No doubt they relied heavily on Premutico’s existing industry relationships to execute this approach, as opposed to spending large sums on brand (& credibility) building campaigns. Perhaps this strategy is one reason they have been able to raise less external capital, yet get closer to profitability in the same timeframe as Mr Yum.

Cap Tables & Runway

Outside of the product offerings, the two companies approaches to capital raising have been quite different.

Mr Yum hit the headlines a couple of times during 2021 raising a ’record-breaking’ $89M Series A (led by Tiger Global), followed shortly after by a top-up round and has raised over $100M to date. The company used the funds to rapidly expand their pre-pandemic team of just 12 people, only to eventually lay off a significant percentage of their team (17% in August 2022 and another 40 in March 2023) in response to tightening market conditions. According to Crunchbase, Mr Yum has attracted investment from around 15 investors, making it quite a stacked cap table. This might be an advantage for them by gaining advice and input from a range of shareholders to partly help them make up for their lack of industry know-how.

It’s unclear from public reports how close Mr Yum is to profitability after a tumultuous last 6 months and with the heat rising from competitors. Long-term success will likely bank on their ability to scale globally, particularly in the UK and US which significantly dwarf the Australian market opportunity.

me&u has been slower out the gate with VC investment, raising only $66M to date from a small handful of key investors (namely Acorn Capital, Robbie Cooke, Tyro Payments and Justin Hemmes). This is perhaps due to Premutico’s ability to leverage funds from his previous company (sold to TripAdvisor for $140M in 2014) in the early days, as well as his industry connections. me&u also made some members of its team redundant as the tech market tightened, however, the total number of redundancies seemed to be much smaller (approx. 20 people), likely because they did not hire as rapidly throughout 2021 and instead focused on bringing in heavy-hitters to their C-suite. Similar to Mr Yum, the company is now focused on dominating overseas markets in order to take the business to the next level and has apparently already gained a decent initial foothold with 120 US locations and over 100 UK locations. Off the back of its latest raise, me&u told the media it is now focused on profitability, targeting the end of the year at the latest, and doesn’t expect to raise again.

Market Share

It’s pretty clear that the market both me&u and Mr Yum are playing in is currently an out-and-out land-grab race. Whether or not they’re racing to grab the same slice of land is yet to be seen.

In the beginning, both companies were working to essentially ‘create’ the category and increase awareness of their solutions, yet post-COVID with the awareness and education piece largely solved at a user level, it's now about who can convince customers that their solution is best, or at least fit-for-purpose for their target buyer segment.

It’s difficult to gauge definitive numbers on each company’s current market share and momentum, as the numbers are generally under lock and key - or at least selectively chosen for public distribution. The best data on me&u available is that provided by an investor update from Acorn Capital last year (2022) which claimed the company has around 70% market share of top pub groups, compared to 20% for Mr Yum. However, this figure naturally does not capture the hundreds of other types of hospitality venues outside of pubs.

The number of venues signed up to each platform is potentially a better measure of comparable success, however, only Mr Yum definitively points to a figure on their website, quoting 5000+ venues.

Ultimately, it will be a combination of both capturing market share and how each company chooses to structure and weight their pricing strategy (e.g. transaction commissions and/or subscriptions) that will determine if either company, or both, can build a sustainable business model.

While the companies are taking somewhat different approaches to gaining market share, it appears (at least from the outside) that based on their very similar product offerings to end users, they should be able to attract similar consumers and hence will continue to be fighting it out on the B2B-sales battlefield for a fair while yet (or will they...? Read on!).

The location of that battlefield, however, is now moving to the UK and US, where both companies face increased competition and complexity. In the UK, the tap-order-pay market is already well-established, as the UK government introduced regulations requiring at-table ordering during the height of the pandemic, leading to a flood of solutions entering the market. The US on the other hand, although perhaps less competitive, has a more hands-on food ordering and payment culture, including service-based tipping, which may pose a higher barrier to conversion for QR code ordering platforms.

What will happen next?

When we first started writing this piece, me&u had just announced their raise and throughout our research, we were left with the question…

“Can these two Aussie start-ups both continue to grow while going head-to-head, staying in their customer segment lanes whilst simultaneously taking the world by storm, will one triumph while the other waivers, or will there be an eventual perfect marriage of the two?”

We’re not going to say we predicted the future, but… since then, there has been much excitement around reported merger talks between the two companies. The likelihood of this happening has only increased with the rivals this week seeking advice from investment banks on what a potential merger might look like.

The AFR has reported that “a potential transaction would likely be structured as a scrip-for-scrip merger” with the result being improved overall cash flow - particularly important in the current tight capital market - and the ability to potentially scale back their international expansions to focus on consolidating their position in the Australian market.

While there’s no guarantee a deal will come to pass, one thing is for sure - we’ll be watching this story closely as the story plays out over the coming weeks!